The Canary in the Coal Mine

In mid-2025, Tata Consultancy Services announced layoffs of 12,200 employees — the largest in the company's history, and a figure that analysts called the start of a broader reckoning for India's $283 billion IT outsourcing sector. TCS attributed the cuts to skill mismatches. Analysts read it differently: as the opening tremor of a structural collapse.

The outsourcing model — where enterprises hand off technology work to vendors who manage it at scale — has been the default global delivery mechanism for three decades. It built TCS, Infosys, Wipro, and HCL into some of the world's largest employers. But those companies are now shedding headcount as the clients they built those businesses serving choose a different model entirely: the AI-enabled Global Capability Center.

This isn't a cyclical dip. The data shows a structural inversion — and understanding why it is happening, and how fast, is essential for any enterprise still operating under the old model.

The Numbers Are Already In

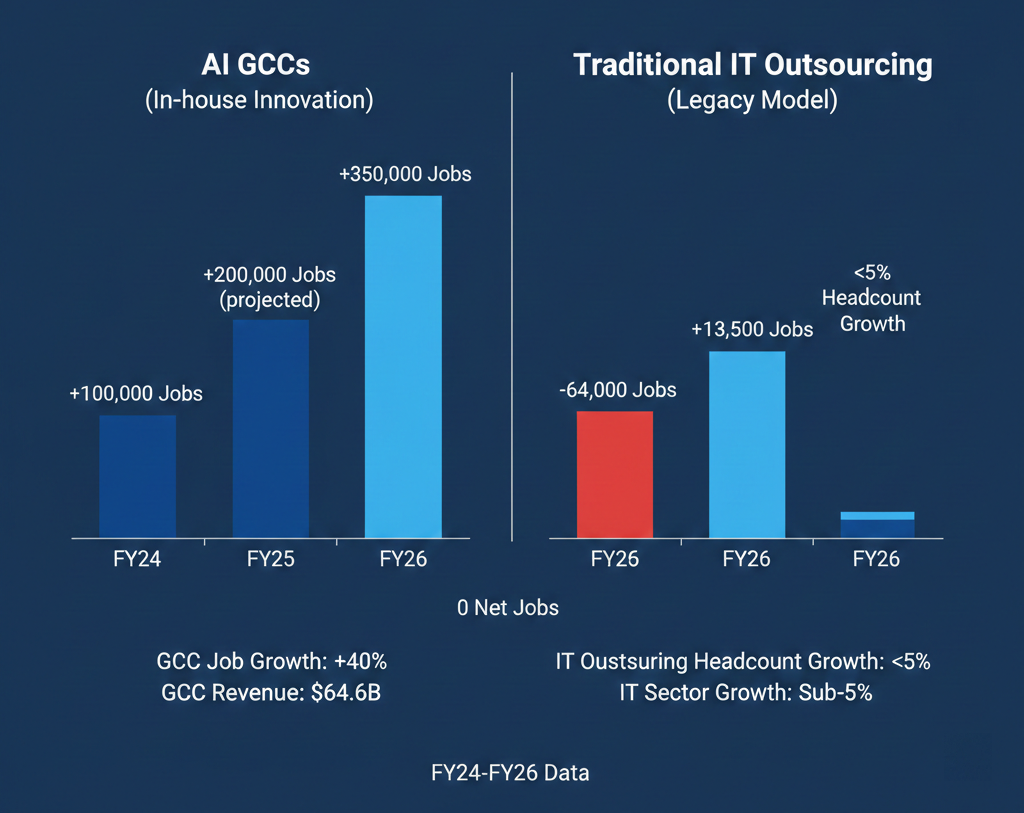

The divergence between the two models is no longer directional — it is measurable and accelerating. In fiscal year 2024, GCCs across India grew at 40% while India's top five IT outsourcing firms reported negative to sub-5% growth. GCC revenue hit $64.6 billion — nearly a quarter of India's total IT sector output — and the trajectory toward $100 billion by 2030 is broadly consensus.

The employment data is equally stark. Indian IT services firms added a net 13,500 jobs in FY2025, following a loss of 64,000 the previous year. Over the same period, GCCs added over 100,000 jobs, with hiring projected to rise 50–75% in FY26 — generating an estimated 3.4 to 3.8 lakh new roles over the next five to six quarters.

Perhaps most telling is the client-side signal from financial services. JPMorgan Chase and Wells Fargo now each employ over 50,000 staff in India — directly, not through IT service vendors. These are not outsourcing arrangements. They are in-house GCCs that rival mid-sized IT companies in headcount, and they answer to a single client: the parent enterprise.

The wider India hiring data corroborates this sector-level shift. Naukri JobSpeak's December 2025 index — tracking over six million job postings — recorded AI/ML role hiring up 53% year-on-year, unicorn company hiring up 21%, and BPO/ITES sector hiring up 20% in Q4 2025. The skills economy is reorienting around precisely the roles GCCs demand — and the volume of that demand is accelerating, not stabilising.

"GCCs grew 40% in FY24 while the outsourcing sector's top five firms managed sub-5%. This is not a market fluctuation — it is a model transition."

The Structural Problem Traditional Outsourcing Can't Fix

The GCC model's rise isn't purely a cost story. If it were, outsourcing firms could simply cut rates and hold ground. What is happening instead reflects a deeper recognition: that the outsourcing model is architecturally misaligned with how enterprises need to operate in an AI-native, product-centric, data-sensitive world.

The Incentive Inversion

Outsourcing vendors are optimised for one thing: maximising billable hours and headcount. Their revenue model depends on volume — the more engineers they deploy, and the longer projects run, the more they earn. This creates a structural misalignment where a vendor's financial interest is to expand scope, extend timelines, and avoid the kind of automation that would shrink their billings. The enterprise, by contrast, wants speed, efficiency, and outcomes.

In a GCC, the incentive structure inverts entirely. The team's performance is measured against the parent company's business outcomes, not against contract SLAs. When an in-house engineer automates a process that saves 200 hours a week, that's a win — not a threat to someone's revenue line.

The IP and Knowledge Problem

When enterprises outsource product engineering, they are building intellectual property on someone else's infrastructure, processes, and institutional memory. Vendor engineers rotate across clients. Domain knowledge that took months to build disappears when a key resource is reallocated. Code reviews, architectural decisions, and product roadmaps happen inside a vendor relationship — and when that relationship ends, the enterprise often cannot fully reconstruct what was built or why.

GCCs eliminate this risk entirely. The team is hired exclusively for the parent company. Knowledge accumulates, compounds, and stays in-house. According to Morgan Lewis's analysis of the GCC rise, IP ownership and data security control are now among the primary factors driving enterprise decisions to move from outsourcing to the GCC model, particularly in regulated sectors.

The Hidden Cost Reality

Outsourcing's cost argument has always relied on a narrow comparison: vendor rate card versus local headcount. In practice, the total cost of ownership is substantially higher. Enterprises routinely encounter vendor management overhead, SLA penalty disputes, scope creep charges, transition costs when switching vendors, and quality remediation costs that never appear in the initial contract. GCCs carry higher upfront setup costs — infrastructure, legal entity, compliance — but their total cost trajectory typically becomes favorable by Year 2 or 3 and improves continuously as the team matures.

Why AI Is Accelerating the Collapse, Not Just Contributing to It

Artificial intelligence doesn't affect the outsourcing and GCC models equally. It creates a structural asymmetry that systematically advantages the GCC model and undermines the outsourcing model's financial foundation.

AI Destroys the Billing Pyramid

Traditional IT outsourcing firms depend on a pyramid: a few senior architects at the top, a broad base of junior and mid-level developers at the bottom. The base is where the margin lives — high-volume, lower-complexity work delivered at scale. AI — specifically code generation, automated testing, and intelligent documentation — attacks this base directly. Junior and mid-level coding, test case generation, and support ticket resolution are precisely the categories where large language models perform at or above human-comparable quality.

For an outsourcing firm, AI-driven automation means fewer billable engineers — a direct revenue reduction. TCS's CEO cited skill mismatch as the reason for the 12,000 layoffs, but the more precise read is that the skills that are mismatched are the mid-level roles AI has made economically unviable to staff at traditional margins.

The labour market confirms this pyramid bifurcation in real time. India's IT roles commanding ₹20 lakh or above grew 42% year-on-year by December 2025 — while mid-level, lower-complexity roles contracted sharply. AI is not merely flattening the outsourcing pyramid; it is eliminating the base that made outsourcing's volume economics viable, leaving only the senior tier that GCCs already capture.

For GCCs, AI Is Amplification

Inside a GCC, AI adoption has the opposite effect. When an engineer is empowered by AI tools, their output expands — they can own more of the stack, ship features faster, and take on architectural decisions they would previously have been excluded from. More than 90% of leading GCCs have launched or expanded AI Centres of Excellence in the last 18 months. These aren't overhead functions — they are operational accelerators embedded in product and engineering workflows.

The contrast is structural. An outsourcing firm that adopts AI must pass the productivity gains back to the client (reducing billings) or absorb them as margin (eliminating the reason to automate). A GCC that adopts AI captures the productivity gains directly — its engineers ship more, the enterprise moves faster, and the competitive advantage compounds internally.

The Infosys Model Inversion

The most pointed illustration of this asymmetry is Infosys's own strategic pivot. In 2025, the company publicly unveiled an AI-first GCC model — a structured approach for transforming GCCs into AI-native innovation hubs. An outsourcing vendor, facing structural decline in its core model, is now selling the infrastructure and methodology for enterprises to build the very GCC model that is displacing it. That is the signal: even the incumbents of outsourcing have recognised that the future is internal.

What the Value Data Actually Shows

The investment case for GCCs has historically rested on cost savings. The 2025 data shows the case is now much stronger than that.

PwC India's research of 120 senior executives across GCCs and their respective headquarters reveals that during FY2020–2024, GCCs generated value at a weighted average CAGR of 10–11% for their parent companies. This figure encompasses cost efficiency, but it is dominated by speed-to-market improvements, innovation contributions, and product ownership capabilities — outcomes that outsourcing contracts structurally cannot deliver.

Deloitte's Global Shared Services Survey reinforces this: over 80% of leading organisations now have GCCs in some form globally. The transition from outsourcing to GCC is no longer a competitive advantage — it is rapidly becoming the baseline for competitiveness.

The Talent Migration That's Making It Permanent

There is a secondary force accelerating the outsourcing-to-GCC transition that rarely features in financial analysis but may ultimately matter more: India's best engineers no longer want to work for IT services firms.

The career trajectory inside an outsourcing vendor typically means rotating across client projects, limited product ownership, and a progression ceiling determined by billing rates rather than engineering depth. GCCs offer the inverse: a single-company culture, exposure to global product decisions, accelerated leadership pathways, and the cultural alignment that comes from working inside the enterprise rather than alongside it. Attrition at GCCs runs at approximately 9% versus 25–30% at IT services firms — a differential that compounds into structural talent depth over time.

India's December 2025 hiring data reinforces the pipeline story. Fresher hiring grew 18% year-on-year, and senior roles at ₹20 lakh and above expanded 27% over the same period. The talent pool — at both entry and experienced tiers — is growing in the direction that feeds GCC capability depth, not IT services headcount. That dual-tier growth is what enables GCCs to build the internal talent ladder that outsourcing vendors have always lacked.

The talent migration is also directional. TCS's layoffs are creating a supply pool of experienced engineers in the market — engineers who are now being absorbed by GCCs rather than by other outsourcing firms. GCCs eyeing 3.8 lakh tech hires in FY26 are picking up mid-career engineers with domain expertise, institutional knowledge, and AI fluency — exactly the talent profile that makes a GCC strategically valuable rather than merely cost-efficient.

"India's best engineers no longer see IT services as a career destination. GCCs are where domain depth, product ownership, and global mandate come together."

What Enterprise Leaders Should Do Now

For organisations still running their core technology work through outsourcing vendors, the strategic question has shifted. It is no longer whether to transition to a GCC model — it is whether the transition is already too late to be first-mover, and how to manage the wind-down of outsourcing dependencies while standing up internal capability.

The Transition Sequence

Enterprise leaders who have navigated this successfully follow a consistent pattern. First, they identify the functions where IP sensitivity and innovation velocity matter most — and begin insourcing those specifically, rather than attempting a wholesale outsourcing replacement. This reduces risk and generates early wins that justify further GCC investment.

Second, they allow the outsourcing relationship to persist for commodity functions — infrastructure maintenance, legacy system support, and high-volume, low-differentiation work - while GCC teams take ownership of new product development and AI-driven initiatives. The hybrid model is a transitional state, not a permanent one: as the GCC matures, the vendor scope contracts.

The Niche Talent Imperative

The most common GCC scaling failure is not strategic — it is operational. Leaders underestimate the difficulty of hiring niche technical roles (AI engineers, cloud architects, data platform specialists) in emerging GCC cities at speed. The talent market for these roles is competitive even in Tier-2 cities, and the time-to-productivity gap for a mid-career hire in a new GCC is typically 60–90 days. Building this pipeline before the need becomes urgent is the difference between a GCC that scales and one that stalls.

The cybersecurity talent gap is a sharp case study in this urgency. India's December 2025 Naukri JobSpeak data shows specialist security hiring growing well above the broader market average — reflecting both the rising compliance burden on GCCs and the acute scarcity of verified practitioners:

• Application Security Engineer: +52% year-on-year hiring growth

• Manager, Information Security: +50% year-on-year

• System Security Engineer: +48% year-on-year

• Security Architect: +43% year-on-year

These are not roles that outsourcing vendors can fill at enterprise grade. They require the institutional context, system access, and continuity that only an embedded, in-house GCC team can provide — reinforcing why the most security-conscious enterprises are among the fastest to move off the outsourcing model.

Conclusion

The traditional IT outsourcing model is not being disrupted by a better outsourcing model. It is being displaced by a fundamentally different architecture — one where the enterprise owns its talent, its IP, its data, and its AI advantage internally. The GCC model's 40% growth against outsourcing's stagnation, the 10–11% value CAGR it delivers, and the accelerating talent migration away from IT services firms are not trends to monitor. They are the current state. The transition window is open — but it is narrowing as early movers compound their advantages every quarter.

Building a GCC that wins on capability rather than just cost requires closing niche skill gaps fast and maintaining hiring quality under growth pressure. Crewscale works with AI GCCs to source and onboard the precise technical talent — from AI engineers to cloud architects — that separates centres that scale strategically from those that grow chaotically. The model has changed. The question now is how quickly your organisation changes with it.